World Economic Situation and Prospects (WESP) is a joint product of the Department of Economic and Social Affairs, the United Nations Conference on Trade and Development and the five United Nations regional commissions. It provides an overview of recent global economic performance and short-term prospects for the world economy and of some key global economic policy and development issues. One of its purposes is to serve as a point of reference for discussions on economic, social and related issues taking place in various United Nations entities during the year.

The World Economic Situation and Prospects update as of mid-2010 highlights that while the world economy continued to improve in the first half of 2010, leading to a slight upward revision in the United Nations outlook for global growth, the pace of the recovery is too weak to close the global output gap left by the crisis. It also points out that the recovery is uneven across countries, with encouraging growth prospects for some developing countries, but lacklustre economic activity in developed economies and below potential growth elsewhere in the developing world. The Report argues that important weaknesses in the global economy remain, and draws attention to some of the policy challenges that need to be addressed to solidify and broaden the recovery.

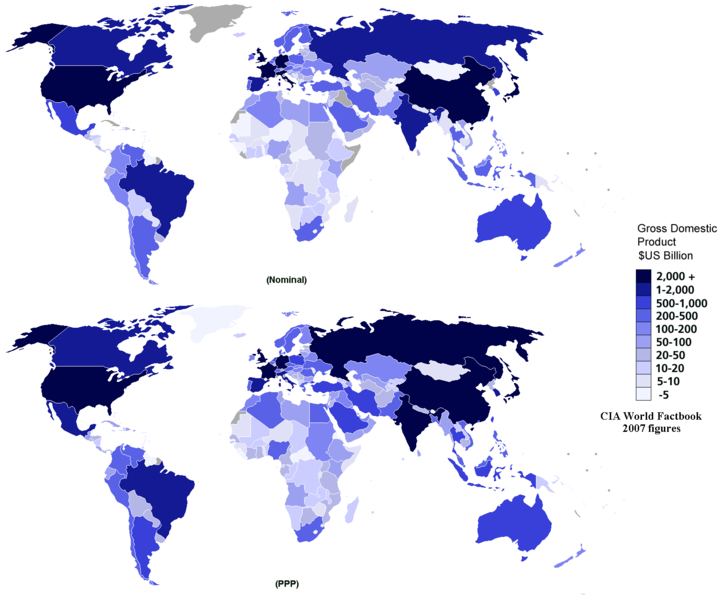

World Economic Situation and Prospects 2010

The world economy is on the mend. After a sharp, broad and synchronized global downturn in late 2008 and early 2009, an increasing number of countries have registered positive quarterly growth of gross domestic product (GDP), along with a notable recovery in international trade and global industrial production. World equity markets have also rebounded and risk premiums on borrowing have fallen.

World gross product (WGP) is estimated to fall by 2.2 per cent for 2009, the first actual contraction since the Second World War. Premised on a continued supportive policy stance worldwide, a mild growth of 2.4 per cent is forecast in the baseline scenario for 2010. According to this scenario, the level of world economic activity will be 7 per cent below where it might have been had pre-crisis growth continued.

The report cautions that despite these more encouraging headline figures, the recovery is uneven and conditions for sustained growth remain fragile. Credit conditions are still tight in major developed economies, where many major financial institutions need to continue the process of deleveraging and cleansing their balance-sheets. The rebound in domestic demand remains tentative at best in many economies and is far from self-sustaining. Much of the rebound in the real economy is due to the strong fiscal stimulus provided by Governments in a large number of developed and developing countries and to the restocking of inventories by industries worldwide. Consumption and investment demand remain weak, however, as unemployment and underemployment rates continue to rise and output gaps remain wide in most countries. In the outlook, the global economic recovery is expected to remain sluggish, employment prospects will remain bleak and inflation will stay low.

The report also highlights a number of risks and uncertainties to the outlook, including a premature exit from the stimulus measures and a hard landing of the dollar due to the renewed widening of the global imbalances. In terms of policy measures, the report recommends continued fiscal stimulus measures in the short run, a continued focus on the rebalancing of economic growth in a number of respects, better policy coordination, strengthened global governance and more decisive reforms of the global financial system.